系好安全带,美国要起飞啦 [美国媒体]

美联储加息三部曲的第一部近在眉睫,何时宣布则取决于美国是否已经做好起飞的准备。自从2009年利率触底,联邦储备局就何时加息反复做出了乐观的预期,但加息日却一直没有来到。

Buckle up

系好安全带

The first of three pieces on the Federal Reserve’s imminent interest-rate decision looks at whether America is ready for lift-off

美联储加息三部曲的第一部近在眉睫,何时宣布则取决于美国是否已经做好起飞的准备。

SINCE interest rates hit rock-bottom in 2009, the Federal Reserve has repeatedly made optimistic forecasts about when they would start rising, only to delay the big day again and again. If the Fed has been a bullish coach, the markets have been trusting fans, continually believing that an increase is imminent, only to have their expectations dashed. At last, however, the moment seems to have arrived. On December 16th, when the Fed’s rate-setting committee meets, it seems all but certain to raise rates.

自从2009年利率触底,联邦储备局就何时加息反复做出了乐观的预期,但加息日却一直没有来到。如果说美联储执牛市之耳,市场为其马首是瞻,始终坚信加息日就在眼前,那么就只会落个期望破灭的下场。不过,这一时刻终于要到来了。就在12月16日,美联储将召开议息会议,届时应该就会宣布加息。

For that, thank the strength of the labour market. Unemployment, at 5%, is as low as most analysts reckon it can sustainably fall. During the recession, America lost 8.7m jobs. It has since gained 13m. In 2010 there were six unemployed workers for every job opening; today there are 1.5.

对此,首先要感谢劳力市场的强劲。超出大多数分析家的预期,失业率竟跌至5%。在经融危机后的衰退中,美国失去了870万个工作岗位。而现在已经创造了1300万个工作岗位。在2010年时,每个工作岗位有6个失业者来竞争;今天则只有1.5人来竞争。

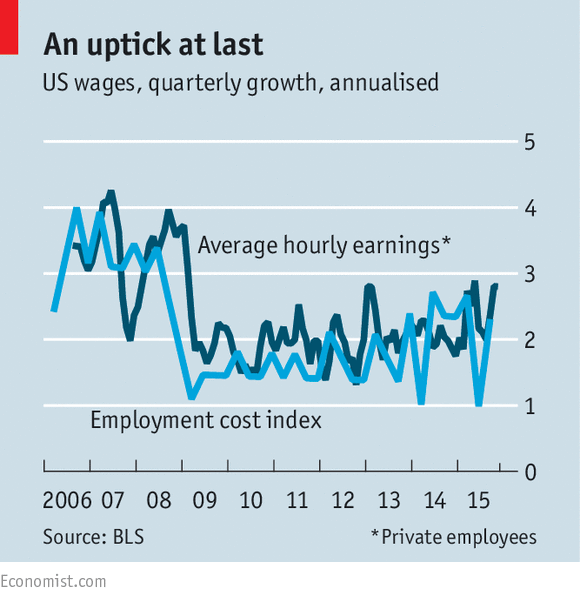

Wages, long stagnant, finally appear to be growing again, too. In September, when the Fed toyed with raising rates, average hourly pay had just grown by 2%, on an annualised basis, over the prior three months. Now that has risen to 2.8% (see chart). By one measure, wages grew by fully 4% in the third quarter of the year. Accelerating pay suggests that slack in the labour market has almost gone.

而停滞许久的工资也终于开始再次上涨。九月份,美联储摆弄了一下加息,就使得平均时薪按前三个月的年率计算上涨了2%。到今天为止,涨幅已经增加到了2.8%(见图表)。通过这么一个措施,今年第三季度工资就上涨了4%。加薪意味着劳力市场的疲软状态已经基本消失。

The pick-up in wages could peter out, however. Since the recession hordes of workers have left the labour force altogether: labour-force participation among 25- to 54-year-olds in the third quarter of the year was lower than at any time since 1984. If some can be tempted back to work, wages will be held down.

但是,工资的回升趋势将会减弱。自从经济衰退以来,大群工人放弃成为劳动力:今年第三季度中,25至54岁人群的劳动参与率已经跌破了自1984年以来的最低点。而如果这些人被吸引回了劳力市场,那么工资就将会停止上涨。

Moreover, the Fed’s preferred inflation measure stands at just 0.2%, well below its 2% target. Cheap oil bears much of the blame. But core inflation, which excludes volatile energy and food prices—and so is a better indicator of underlying price pressures—is only 1.3%.

再者,美联储最爱的通膨指数仅为0.2%,远低于2%的目标值。低廉的油价是罪魁祸首。但是,即使不考虑能源和食品价格的波动,得到的更能说明潜在价格压力的核心通膨指数,也仅为1.3%而已。

Janet Yellen (pictured), the Fed’s chair, chalks up some of the shortfall to a strong dollar making imports cheap (the greenback is up by 19% since mid-2014). That effect should dissipate if the dollar’s ascent stops. There is also less scope for the oil price to plunge, having already fallen by almost two-thirds over the past year. This suggests inflation may pick up in 2016. That, in turn, argues for a rate rise soon, since monetary policy is thought to have only a delayed impact on the economy.

美联储主席珍妮特·耶伦(见照片)将这些问题归因为美元升值造成的廉价进口物(自2014年中以来,美元升值达19%)。一旦美元停止升值,造成的影响就会消退。由于去年以来,油价已经跌了三分之一,所以油价以后的下跌空间很小。这意味着通胀率有望在2016年增长。相应地,由于现在的货币政策已经对经济产生了延迟冲击,所以要求上调利率的呼声响亮。

The Fed is in a jam, though, because it faces asymmetric risks. If it raises rates too soon, its scope to cut them, should the economy then sour, is limited by the fact rates cannot fall far below zero. If it waits until inflation is stronger, it has unlimited capacity to raise rates to tame it.

不过,美联储面临着不对等的风险,正处在困境之中。如果升息动作过大,当经济恶化时,由于利率不得低于0,降息的范围就会被制约。而如果等到通胀率上涨再加息,那么届时美联储的调控能力将不再受到任何制约。

Getting this balance right will be tricky. Ms Yellen likes to emphasise that starting early keeps the journey smooth; abrupt rises later might rattle markets. Yet the Fed’s forecast for rates is steeper than what the market predicts. The Fed’s median rate-setter expects interest rates to rise to around 1.5% by the end of 2016; by contrast, traders expect rates of only 0.85% in a year’s time.

如何在实际操作中取得平衡是一件难事。耶伦女士强调,尽早开始这个措施,可以让过程更平缓;突然地加息可能会扰乱市场。尽管如此,美联储对利率增幅的预计仍超过了市场的预期。美联储期望利率在2016年底前升至1.5%;一直相对,交易员则期望利率每年仅增长0.85%。

Two roads in a wood

树林中的分岔路

Who is right depends on how the economy reacts to the first rise. That is hard to predict, because the channels through which monetary policy works are mysterious. Take consumption, which has driven America’s recent growth. The impact of rates on consumer spending is muted by the fact that, unlike in much of Europe, most American mortgages come with fixed interest rates, shielding many Americans from swings in monetary policy. The first rate rise will nudge up the cost of borrowing, but only very slightly.

究竟谁是对的取决于第一次加息后经济的反应。因为货币政策作用通路是复杂而神秘的,难以预测将对经济产生怎样的影响。美国近来的发展是被消费推动的。与欧洲不同,基本上美国人抵押贷款的利率是个定值,在货币政策发生改变时可以减少美国人所收到的冲击,因此消费者的购买力度一般不会受到影响。尽管第一次加息会使得借贷成本上升,但是增幅将会极小。

Nor is a rate rise likely to slow investment much. The evidence for the responsiveness of investment to rates is mixed; business confidence is probably more important. If—as some think—a rate rise is a signal from the Fed that America’s economy is healthy, investment could even rise.

加息也并不会减缓投资。投资行为受利率的影响是复杂的;影响投资行为更重要的因素是商界的信心。如果——就像有人认为的那样…——加息是美联储释放的美国经济复苏的信号,那么投资行为将会增加。

That leaves exports. If rising rates cause the dollar to appreciate further, American goods will become still more expensive abroad. America’s embattled manufacturers will not welcome that (a recent survey suggests manufacturing output shrank in November for the first time in three years). But another surge in the dollar is unlikely, since a rate rise in December is now widely expected.

而对于出口的影响在于,如果加息使得美元进一步增值,那么美国产品在国外将会卖得更贵。处于商战中的美国制造商将不会希望这种情况发生(最近调查显示,11月的制造业出口额在过去三年中第一次缩水)。但是这也未必,因为希望12月加息的呼声是如此广泛。

If the Fed follows through on its forecasts, though, and raises rates faster than markets expect in 2016, the dollar may well rise further, dampening inflation quickly. Stanley Fischer, the Fed’s vice-chair, recently estimated that a 10% rise in the dollar reduces core inflation by half a percentage point within six months. For all her horizon-gazing, Ms Yellen is unlikely to persist with rapid rate rises if they push inflation too far below target in the short term.

如果美联储按照自己的预计行事,在2016年中加息幅度高于市场预期,使得美元进一步升值,那么将会迅速抑制通膨。美联储副主席Stanley Fischer近来作出估计,认为美元升值10%就会使得核心通胀率在6个月中降低0.5%。耶伦一旦看到如此远景,则不会坚持快速的加息,以免在短期内将通胀率降得远低于目标。

Further falls in commodity prices could also keep the brakes on. This would drag down inflation directly, but could also reduce it indirectly by pushing up the greenback. Much of the dollar’s recent appreciation, on a trade-weighted basis, derives from weakness in the Mexican peso and the Canadian dollar. Those currencies weaken when commodity prices fall, argues Paul Ashworth of Capital Economics.

而未来物价也会停止下跌。这将会直接拉低通胀率,同时通过促使美元升值而间接减少通胀。美元最近的升值,从贸易权重的角度来讲,源于墨西哥比索和加元的疲软。资本经济的Paul Ashworth认为,在物价下跌时,这些货币就会疲软。

Most uncertain of all is where interest rates will end up. That depends on the so-called “natural” rate of interest; the sweet-spot which balances demand and supply. This is tricky to pin down, but it is commonly thought to be falling, in part due to systemically slower growth since the crisis. One estimate—based on work by John Williams, a rate-setter himself—puts the inflation-adjusted natural rate of interest at -0.1%, down from 3.1% in 2000. Given an inflation target of 2%, that points to rates eventually settling at just under 2%. That is worryingly low; in 2007, before the crisis, the Fed had leeway to cut rates by over 5 percentage points.

而最难以判断的是,加息将在何时停止。这取决于所谓的“自然”利率;即供需达到平衡时的利率水平。这一利率指难以确定,不过被普遍认为由于经济危机造成的系统性经济发展减缓的缘故而下跌。有一种估测认为——基于美联储利率设定官员John Williams的研究基础——受通胀率影响的自然利率为-0.1%,而该值在2000年时为3.1%。而通胀率的目标被设定为2%,最终通胀率将被控制在略低于2%的位置。这个值已经低到了令人忧心的程度;2007年时,在经济危机之前,美联储的降息余地在5%以上。

The last time monetary policy changed in a comparable way was in 1947, when the Fed started raising rates from a lowly three-eights of a percent, where they had sat for five years. This time, the wait for another stint near zero may not be nearly so long.

最近一次能与之相提并论的货币政策调整发生在1947年,当时的利率为3/8个百分点,已经保持了五年,美联储由此开始加息。而这一回,或许用不了多久就能再次接近零点。

版权声明

我们致力于传递世界各地老百姓最真实、最直接、最详尽的对中国的看法

【版权与免责声明】如发现内容存在版权问题,烦请提供相关信息发邮件,

我们将及时沟通与处理。本站内容除非来源注明五毛网,否则均为网友转载,涉及言论、版权与本站无关。

本文仅代表作者观点,不代表本站立场。

本文来自网络,如有侵权及时联系本网站。

图文文章RECOMMEND

热门文章HOT NEWS

-

1

Why do most people who have a positive view of China have been to ...

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

推荐文章HOT NEWS

-

1

Why do most people who have a positive view of China have been to ...

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10